What Is TDS?

TDS is among the tax collecting methods in which a individual making or crediting a charge to another needs to subtract a certain proportion of the value from that sum. TDS is like a cash tax charge to the state. It’s in preparation. The sum of the TDS shall be paid by the Deductors to the Treasury. Account up until the 7th of the next month in which the balance is withdrawn. As the TDS is being paid by the Deductors to the Treasury. The Accountant shall ensure the daily inflow of cash capital to the State at appropriate intervals.

What Is Liable For The Exclusion Of Root Tax (TDS)?

The Income Tax Act allows defined individuals to subtract tax for some forms of payments made by them. The list of these individuals needing the development of TDS is specified in the TDS section set out below. The following are the specified person who is liable to deduct TDS.

- An Individuals or an H.U.F. is not liable to deduct TDS on such payment except where the individual or H.U.F. is carrying on a business/profession where accounts are enforce to be audited u/s 44AB, in the immediately preceding financial year.

- . An individual is responsible to have audited his or her accounts 44AB if, throughout the applicable financial year, his or her gross sales, turnover or gross receipts exceed Rs. 2 crore (Rs.60 Lacs for A.Y.2012-) in the case of a business or Rs. 50 Lacs (Rs. 15 Lacs for A.Y. 2012-) in the case of a profession.

TAX DEDUCTION AND COLLECTION ACCOUNT NUMBER (TAN)

TAN is an alpha numeric 10 digits number. Every person who is accountable to deduct tax at source must obtain TAN no. from the department in form no. 49B within one month from end of the month in which tax was deducted. TAN is needed to be mention on every transaction related to TDS. There is a penalty of Rs. 10000 on failure to apply TAN

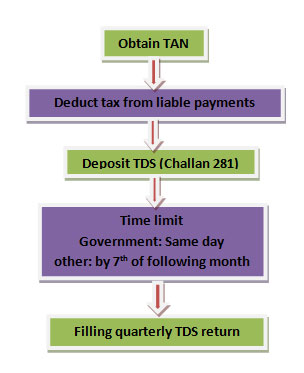

Procedure to pay TDS

Due Date of deposit of Challan 281 and filling quarterly return of TDS

Every person who is accountable to deduct TDS shall deposit the TDS deducted by him by 7th of following month in which TDS is deducted however Due date of deposit of TDS for the month of March is 30th April

The deadline of the quarterly TDS return is 15th of the next month in each year, although this deadline could be 15th in the case of the quarter ended March 20XX

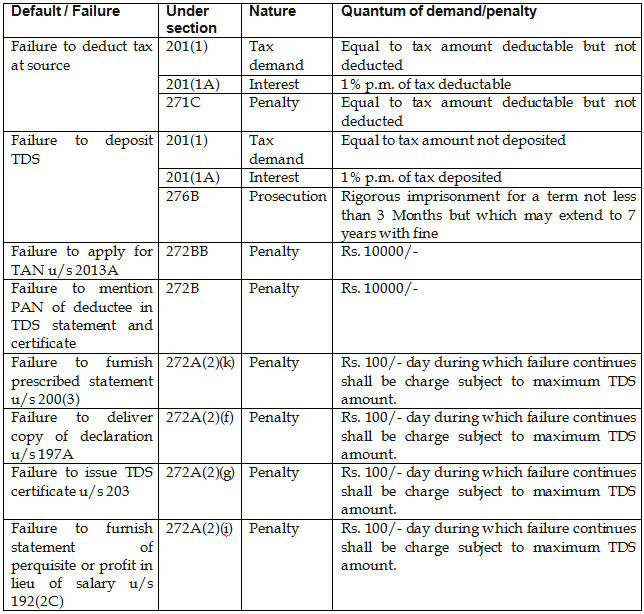

TDS Defaults

- Failure to deduct whole or part of TDS

- Failure to deposit whole or part of TDS

- Failure to apply TAN within prescribed time

- Failure to furnish various certificates/forms/return within prescribed time

- Failure to mention PAN no. of the deductee

- Variation between amounts mentioned in TDS return and amount as per TDS Challan u/s 281.

Penalties and interest in the event of non-filling / non-deduction and late deposit of the TDS sum.